To get a home equity credit line, you must meet certain conditions. You must have a minimum of 660 credit score, adequate income, and a lifetime HELOC limit. Also, you must meet the lender's loan to-value and debt-to–income ratios.

HELOC requires a minimum credit score of 660

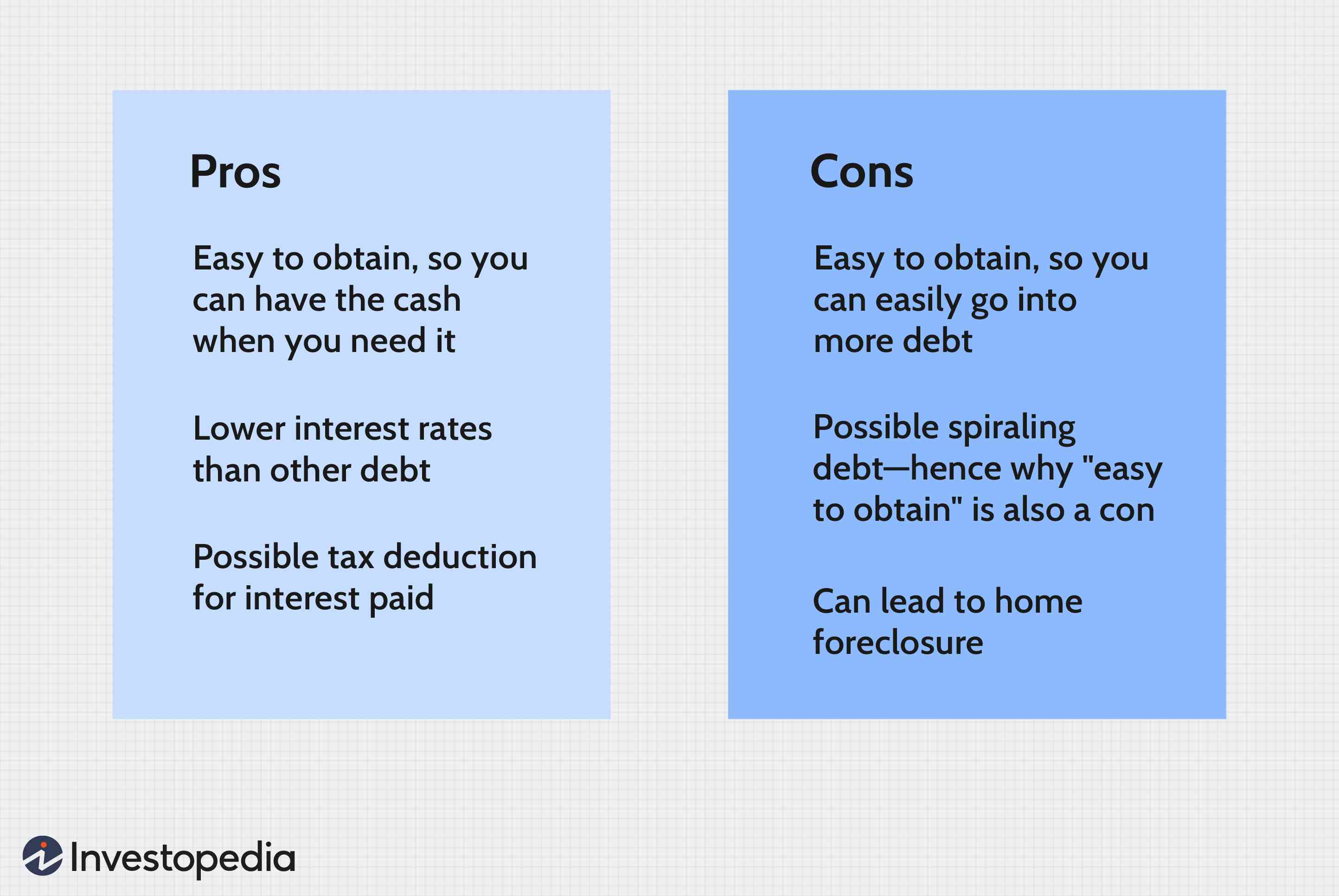

A good credit score is required to get a HELOC. This varies from one lender to the next. Most lenders require that you have a credit score of at least 660. A high credit score can help you qualify for lower interest rates. Lenders may also ask for proof of your income and employment. The lender will use these details to calculate your ratio of debt-to income.

HELOCs can be very expensive. Lenders earn money through fees. These fees pay for their expenses in processing the loan. Lenders may charge closing costs up to 6% of loan amount. If you're looking to borrow $100,000 from your home equity you might need to pay $2,000-$6,000 in closing fees. The lender should be able provide a detailed estimate of total closing costs.

A HELOC loan requires an adequate income

HELOC loans allow you to borrow against the equity of your home. This type of loan can be obtained through many lenders. There are different requirements that lenders may require to be eligible for this type of loan. Typically, you must have 15% to 20 percent equity in your home.

The HELOC loan amount depends on your credit score. Your credit score is a measure of your ability to repay the loan. A high credit score will result in a lower interest rate. When deciding whether you are a good risk, lenders consider your payment history. A credit score of 620 or higher will get you the best rates.

Lifetime limit on HELOCs

HELOC (Home Equity Line of Credit), is a type of revolving credit that leverages the equity in your house as collateral. You don't have to make monthly payments and you can borrow as much money as you need. This credit can be used for any financial purpose, even to pay off credit cards. The credit line will be paid back in the same way as a credit-card bill. You can also draw it down again and again as you need. As long as the credit is paid back on time and you don't exaggerate your credit, this line of credit can be used as often as necessary.

You will need to have all your financial documentation before you apply for a HELOC. These documents will include proofs of income and employment. Also, you may need to pay for a new home appraisal. A fresh appraisal is required before you apply for a HELOC. Home values have increased dramatically in recent years. Depending on the lender, closing a HELOC can take up to thirty days.

Application fee

There are a variety of fees involved with HELOCs. You may have to pay transaction fees to withdraw money from the account. Others might charge you early termination or inactivity fees. Premature closing of an account may result in fees. The fees charged will vary depending on the HELOC type applied for and the lender.

HELOC application fees range from $0 to $500. These fees are typically included in the total cost for the loan and can vary greatly. HELOC lenders sometimes charge loan origination fees. This is the cost of the HELOC process. These fees may be flat-rates or based upon a percentage of the credit line you are approved for.

FAQ

How long does it take for my house to be sold?

It depends on many different factors, including the condition of your home, the number of similar homes currently listed for sale, the overall demand for homes in your area, the local housing market conditions, etc. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

How can I calculate my interest rate

Market conditions influence the market and interest rates can change daily. The average interest rate over the past week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

How can I find out if my house sells for a fair price?

If you have an asking price that's too low, it could be because your home isn't priced correctly. A home that is priced well below its market value may not attract enough buyers. Get our free Home Value Report and learn more about the market.

How many times do I have to refinance my loan?

It all depends on whether your mortgage broker or another lender is involved in the refinance. In either case, you can usually refinance once every five years.

Is it possible fast to sell your house?

It may be possible to quickly sell your house if you are moving out of your current home in the next few months. However, there are some things you need to keep in mind before doing so. First, you will need to find a buyer. Second, you will need to negotiate a deal. Second, prepare your property for sale. Third, you must advertise your property. You should also be open to accepting offers.

What is a "reverse mortgage"?

A reverse mortgage is a way to borrow money from your home without having to put any equity into the property. You can draw money from your home equity, while you live in the property. There are two types: conventional and government-insured (FHA). If you take out a conventional reverse mortgage, the principal amount borrowed must be repaid along with an origination cost. If you choose FHA insurance, the repayment is covered by the federal government.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

The first step in moving to a new location is to find an apartment. This process requires research and planning. This involves researching neighborhoods, looking at reviews and calling people. While there are many options, some methods are easier than others. The following steps should be considered before renting an apartment.

-

Online and offline data are both required for researching neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Online sources include local newspapers and real estate agents as well as landlords and friends.

-

Read reviews of the area you want to live in. Yelp and TripAdvisor review houses. Amazon and Amazon also have detailed reviews. You may also read local newspaper articles and check out your local library.

-

For more information, make phone calls and speak with people who have lived in the area. Ask them about what they liked or didn't like about the area. Ask for their recommendations for places to live.

-

Check out the rent prices for the areas that interest you. If you think you'll spend most of your money on food, consider renting somewhere cheaper. On the other hand, if you plan on spending a lot of money on entertainment, consider living in a more expensive location.

-

Find out more information about the apartment building you want to live in. What size is it? What price is it? Is it pet-friendly What amenities is it equipped with? Are there parking restrictions? Are there any special rules that apply to tenants?