Refinancing homeowners who intend to stay in their homes for at least one year is a great option. They can lower their interest rates and pay less monthly. On the other hand, a home equity loan is a better choice for homeowners who need the money for specific reasons.

Refinance with cash-out

Both home equity loans and cash out refinances can be great options for home-owners with excellent credit ratings and lots of equity. These loans let homeowners access their equity. This equity has grown through regular mortgage repayments and an increase in their homes' value. A cash-out refinance is available to home owners with at least 20 percent equity, which they can use for any purpose.

The interest rate is what makes a cash-out refinance different from a home equity loan. A cash-out loan will lower your monthly cost by $100 if the interest rates are lower than current rates. The amount you can borrow is restricted. People who plan on staying in their homes for several decades will find cash-out refinances more attractive. If you are planning to move soon, a cash-out refinance may not be the best option. It also comes with new fees and closing costs, which may not be recouped after a few months.

Home equity loan

The refinancing vs. the home equity loan comparison is for homeowners who are looking to increase the property's value. Both options have similar features, including low interest rates, minimal value requirements, and monthly payment. The main difference between them is that a refinance will require a second mortgage. You must have more equity in your house. A home equity loan, in contrast, requires only one mortgage payment, and the lender pays for most fees associated with it.

A home equity loan is more convenient for borrowers who want to have one monthly payment rather than several. Additionally, it's an excellent choice for borrowers who have advanced in their amortization schedule. You may have to borrow more, but this option can be cheaper than home equity loans.

Refinance

You can access the equity in your house by refinance or home equity loan. Refinances are where you refinance your existing mortgage. You pay the difference in the loan while a home-equity loan uses your home's equity as collateral. Both options have their advantages and disadvantages, and deciding which one is right for you can be difficult. Although both options can offer you lower monthly payments, the best one depends on your situation and budget.

The principal difference between a loan refinance or a home equity loan is how much money you can borrow. A refinance allows for a larger loan amount, but a loan to fund your home equity will add another monthly payment to your mortgage. The home equity loan has better interest rates.

HELOC

A home equity loan is a way to borrow money from your home, without having to refinance. This loan has lower interest rates and closing costs than unsecured personal loans. Your home is the collateral for home equity loans. If you default on the loan, the lender can take your home. You can choose between a fixed rate mortgage or a home equity loan.

Different draw periods are available for home equity loans. The first offers a lump sum at the closing, which can be used for home improvements. The latter allows you to draw from a credit line as necessary. However, interest will be charged only during the draw period. Credit limits must not be exceeded.

FAQ

What should I do before I purchase a house in my area?

It depends on the length of your stay. It is important to start saving as soon as you can if you intend to stay there for more than five years. You don't have too much to worry about if you plan on moving in the next two years.

How many times may I refinance my home mortgage?

It all depends on whether your mortgage broker or another lender is involved in the refinance. In either case, you can usually refinance once every five years.

Do I need flood insurance?

Flood Insurance covers flooding-related damages. Flood insurance protects your belongings and helps you to pay your mortgage. Learn more about flood coverage here.

What are the benefits of a fixed-rate mortgage?

Fixed-rate mortgages guarantee that the interest rate will remain the same for the duration of the loan. You won't need to worry about rising interest rates. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

Is it possible to get a second mortgage?

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

What's the time frame to get a loan approved?

It is dependent on many factors, such as your credit score and income level. Generally speaking, it takes around 30 days to get a mortgage approved.

How long does it take for my house to be sold?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It may take 7 days to 90 or more depending on these factors.

Statistics

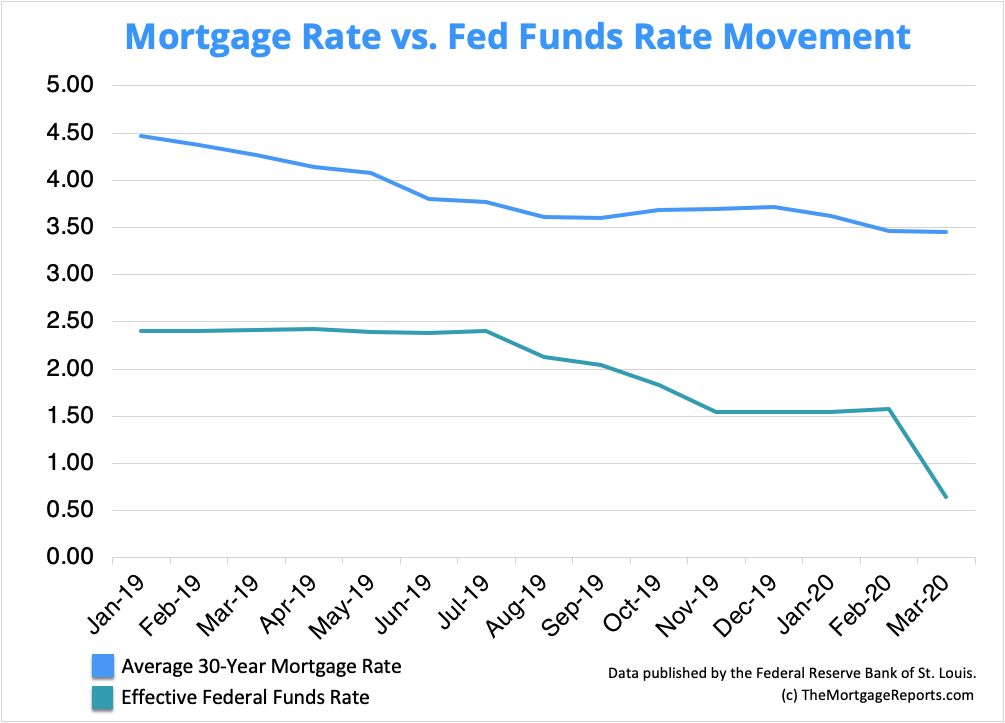

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to Locate Real Estate Agents

The real estate agent plays a crucial role in the market. They help people find homes, manage their properties and provide legal advice. Experience in the field, knowledge about your area and great communication skills are all necessary for a top-rated real estate agent. You can look online for reviews and ask your friends and family to recommend qualified professionals. Local realtors may also be an option.

Realtors work with sellers and buyers of residential property. A realtor helps clients to buy or sell their homes. As well as helping clients find the perfect home, realtors can also negotiate contracts, manage inspections and coordinate closing costs. Most realtors charge a commission fee based on the sale price of the property. Unless the transaction closes however, there are some realtors who don't charge a commission fee.

The National Association of REALTORS(r) (NAR) offers several different types of realtors. To become a member of NAR, licensed realtors must pass a test. Certified realtors are required to complete a course and pass an exam. Accredited realtors are professionals who meet certain standards set by NAR.