You should be familiar with the basics of a mortgage before you apply. This includes the interest rate, downpayment, assessment by the lender, and your personal information. It is important to choose the right mortgage for your home purchase. It can make an enormous difference in your quality life and your finances.

Rate of interest

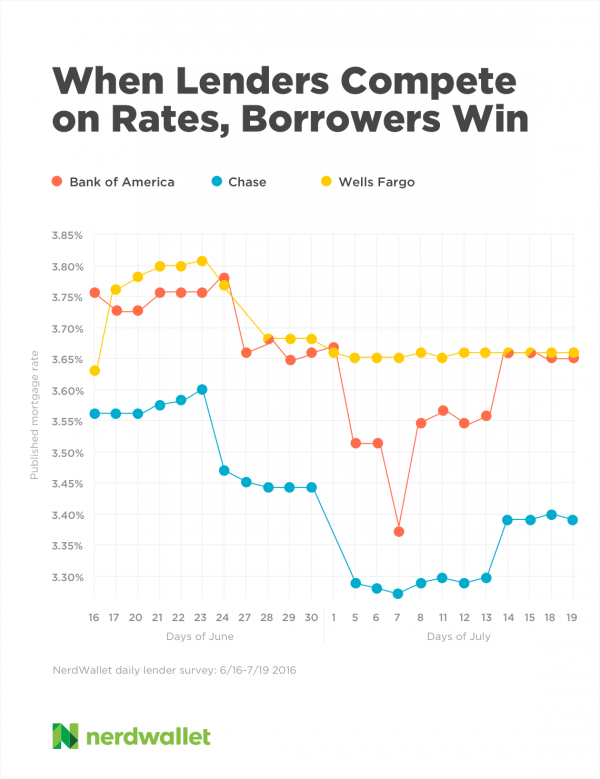

The interest rate on a mortgage is a percentage of the total loan amount. The interest rate is paid by the borrower in addition to the agreed loan repayments. Choosing the right mortgage interest rate is crucial for a person to be able to make their monthly payments. The mortgage interest rate can go up or down, so it is crucial to be on the lookout for changes.

Other costs related to the mortgage, such loan origination fees and discounts points, are not included in an interest rate. Also included are closing costs and mortgage insurance. The APR is intended to give borrowers a clear picture of the total cost of borrowing.

Deposit payment

The down payment on a mortgage is a percentage of the total value of the home that the borrower pays up front. It usually ranges from ten to fifty percent. The mortgage interest rate will be determined by the amount of the down payment that a borrower makes. Generally, the larger the down payment, the lower the interest rate will be. A large down payment reduces the risk of banks lending mortgages.

There are no hard and quick rules about how much down you should pay, but there are some things you can consider when you are deciding on your down payment. A low down payment can be risky so aim for at least 50 percent. A bank is more likely to lend money to borrowers who can put up fifty to sixty percent of the purchase price. If your down payment is low or you don’t have savings, banks will not lend money to you.

Lender's assessment about your information

A mortgage lender looks at many different factors to determine whether you're a good risk. They will examine your credit history and any recent debt applications. These details might be verified with your employer. They'll also look at your payment history, checking to see if you've been on time on your payments and if you've had any late payments. They will also examine any substantial assets you may have.

Lenders are interested in knowing if you can repay the loan. Lenders may also consider your creditworthiness or ability to manage more debt. To determine this, they check the five C's of credit: character, capacity, capital, collateral, and conditions.

Different types of mortgages

There are many different types of mortgages. The first type is known as a conventional mortgage. Conventional mortgages are available for all types of property. These types of loans are backed by the government and are generally easier to qualify for. These mortgages are usually better for first-time home buyers and people with lower credit scores and higher debt-to-income ratios.

An adjustable-rate mortgage is also known as an ARM. Adjustable-rate mortgages are a great choice for people who like to make changes to their interest rates. Another type of loan is a government-backed one, such an FHA, VA or USDA mortgage.

Refinancing options

There are many options when it comes to refinancing your mortgage. It is important that you shop around in order to get the best deal. The current interest rate is one of the biggest factors, so you should contact several lenders before deciding to refinance. You can also consult an attorney to assist you in the process.

Refinancing allows you to take advantage of the equity in your home. It can reduce your monthly payment and make it easier to meet your financial goals. Refinance your mortgage for a variety of reasons.

FAQ

Can I buy my house without a down payment

Yes! Yes. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. You can find more information on our website.

How much does it cost to replace windows?

Window replacement costs range from $1,500 to $3,000 per window. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

How do I calculate my interest rates?

Market conditions affect the rate of interest. The average interest rate during the last week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

What is reverse mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It works by allowing you to draw down funds from your home equity while still living there. There are two types: conventional and government-insured (FHA). With a conventional reverse mortgage, you must repay the amount borrowed plus an origination fee. FHA insurance covers your repayments.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to Find Real Estate Agents

Agents play an important role in the real-estate market. They are responsible for selling homes and property, providing property management services and legal advice. Experience in the field, knowledge of the area, and communication skills will make a great real estate agent. Online reviews are a great way to find qualified professionals. You can also ask family and friends for recommendations. Local realtors may also be an option.

Realtors work with buyers and sellers of residential properties. It is the job of a realtor to help clients sell or buy their home. A realtor helps clients find the right house. They also help with negotiations, inspections, and coordination of closing costs. A commission fee is usually charged by realtors based on the selling price of the property. Unless the transaction is completed, however some realtors may not charge any fees.

There are many types of realtors offered by the National Association of REALTORS (r) (NAR). NAR membership is open to licensed realtors who pass a written test and pay fees. The course must be passed and the exam must be passed by certified realtors. NAR has set standards for professionals who are accredited as realtors.