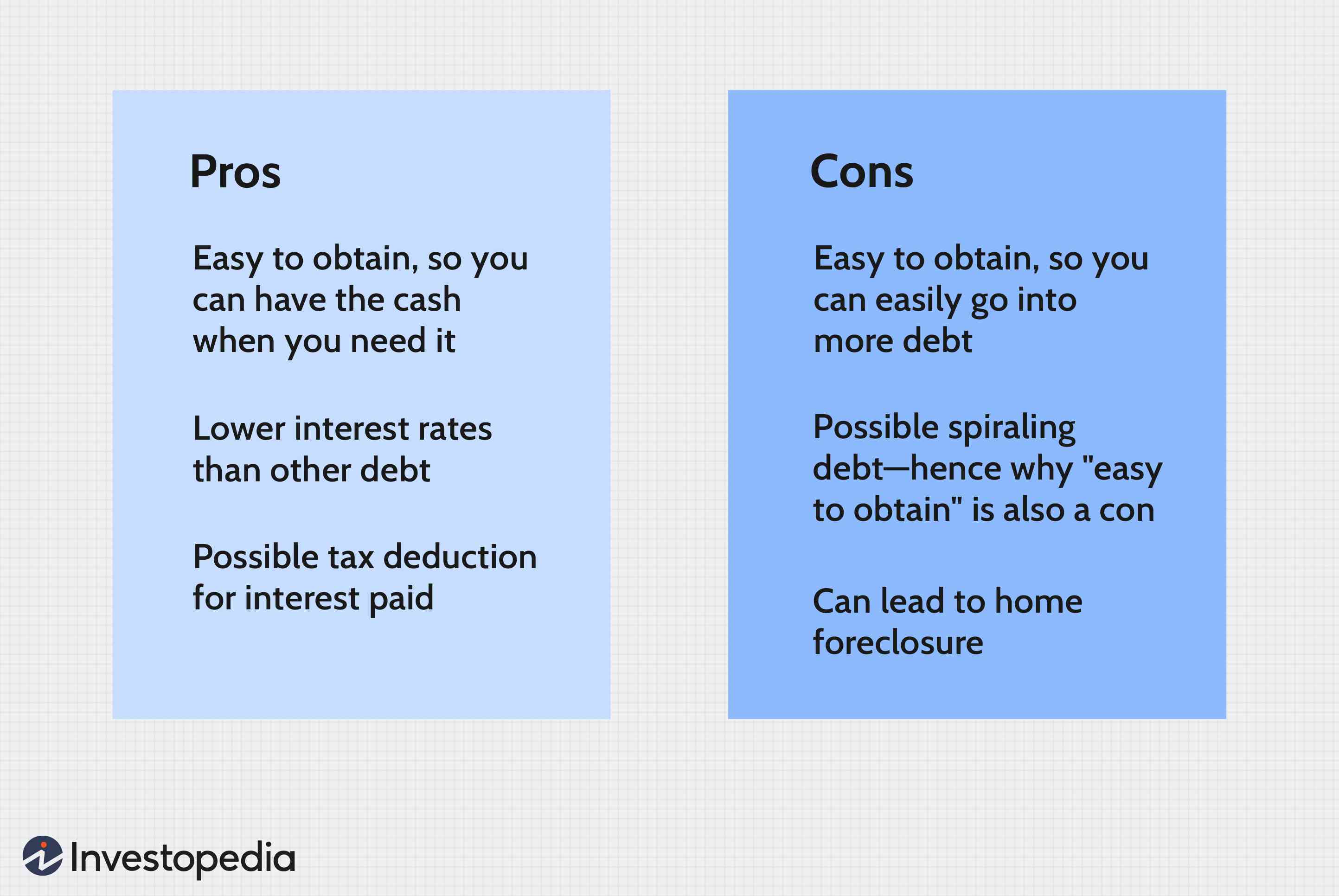

A type of mortgage called the 80-10-10 loan allows borrowers with less than 20% down payment to get rid of PMI. It allows them to buy high-priced homes without having to take out a larger loan. However, the main disadvantage of this type of loan is that it requires taking out two mortgages at the same time.

Piggyback Loans

Piggyback loans, a type mortgage that allows for a lower down payment for your new home, are available. Contrary to other types, the 80-10-10 mortgage only requires that you put down 10% of the total value of your home. You will need to pay mortgage insurance. But if you have good credit and don't mind the added cost, then this mortgage loan is a great option.

A piggyback loan consists of two types of liens: the first lien is a fixed rate mortgage covering up to 80% of the home's purchase price, while the second lien is a home equity line of credit (HELOC). Home equity loans of credit (HELOCs), are similar to credit card but do not charge interest and can be paid off at any moment.

Jumbo loans

The 80-10-10 loan allows borrowers to buy a bigger home with a lower down payment. This allows them to avoid the strict guidelines that are involved with jumbo loans. The monthly payment will be significantly reduced by not having to pay 20% of your home's value. They can instead pay as low as 10%. These loans are also ideal for people in a financial bind and those who are not able to afford the higher down payment required for a conventional loan.

The loan limits for jumbo loans vary by lender, but typically exceed $647,200. The limit for Hawaii, Alaska, and other states is $970,000.800

80 10 10 loans

An 80/10/10 Loan is an option if your goal is to purchase a luxurious home. These loans allow you borrow up to 80% of your purchase price. However, a small downpayment of 10% is required. Additionally, these loans do not require mortgage insurance.

These loans are an attractive option for homeowners looking to avoid jumbo debt, reduce PMI, or buy a house after selling their old one. These loans are similar to piggyback loans. Although there are many variations of this loan, the principle is the same. The basic idea is that you take out two loans. One to your new home and another for your current residence. After you have paid off the first loan, the second one is paid off. This type of loan has the advantage that you can purchase a more expensive home without having to pay PMI.

Rural loans

Rural housing loans can be a great way of purchasing a home. These loans are guaranteed by the USDA and are great for those with low income. This government program offers low interest rates with 0% down payments. It provides guidance to homebuyers on the application process, eligibility requirements, and how to apply. It also offers refinancing for qualified loans.

There are many reasons rural housing loans could be used. They can help buyers purchase their first home or second home. For example, an FHA mortgage requires only 3.5% of the purchase price. This allows individuals with low incomes and lower incomes to afford a mortgage with lower monthly payments.

USDA loans

You might consider a USDA 80-10-10 mortgage if you're in dire need of a home loan with zero down. This program is specifically designed for low and moderate-income households. To be eligible, you must meet certain income requirements and property requirements. If you meet the above requirements, you will be able purchase a property.

There are many options available for this loan program, including bank-owned and self-serviced loans. These loans are guaranteed to have a low interest rate and flexible repayment terms because they are backed USDA. These loan programs also require zero down payment and can be repaid over 33 to 38 years, depending on your income.

FAQ

How can I calculate my interest rate

Interest rates change daily based on market conditions. The average interest rate over the past week was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

Can I buy a house without having a down payment?

Yes! There are programs available that allow people who don't have large amounts of cash to purchase a home. These programs include government-backed mortgages (FHA), VA loans and USDA loans. More information is available on our website.

What are the benefits associated with a fixed mortgage rate?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. You won't need to worry about rising interest rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

How can I repair my roof?

Roofs may leak from improper maintenance, age, and weather. Roofers can assist with minor repairs or replacements. For more information, please contact us.

Is it possible fast to sell your house?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. There are some things to remember before you do this. First, find a buyer for your house and then negotiate a contract. Second, prepare your property for sale. Third, your property must be advertised. You should also be open to accepting offers.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

When moving to a new area, the first step is finding an apartment. This requires planning and research. It involves research and planning, as well as researching neighborhoods and reading reviews. This can be done in many ways, but some are more straightforward than others. These are the steps to follow before you rent an apartment.

-

Researching neighborhoods involves gathering data online and offline. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Local newspapers, real estate agents and landlords are all offline sources.

-

You can read reviews about the neighborhood you'd like to live. Yelp, TripAdvisor and Amazon provide detailed reviews of houses and apartments. You can also find local newspapers and visit your local library.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them what the best and worst things about the area. Ask if they have any suggestions for great places to live.

-

Be aware of the rent rates in the areas where you are most interested. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out more information about the apartment building you want to live in. What size is it? How much is it worth? Is it pet friendly What amenities do they offer? Are you able to park in the vicinity? Are there any rules for tenants?